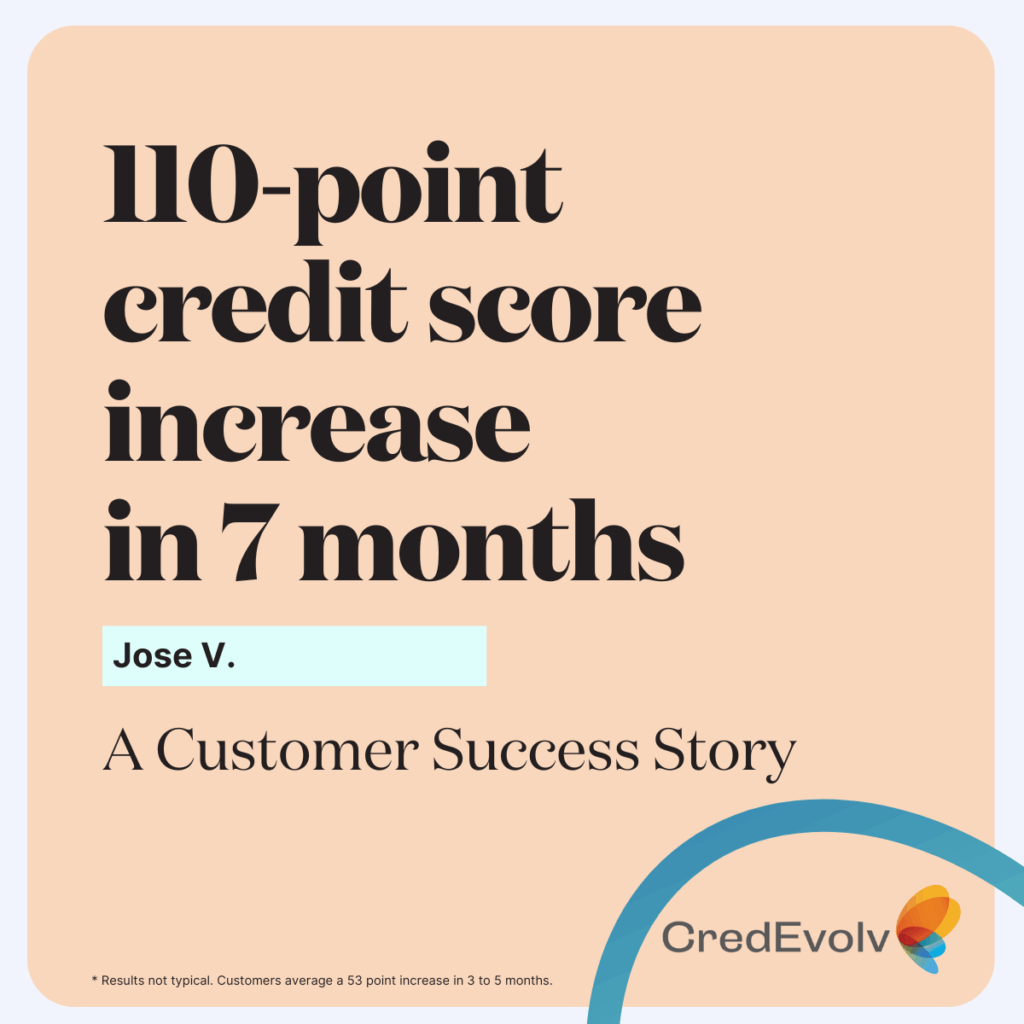

When it comes to unlocking financial opportunities, your credit score plays a powerful role. For Jose, getting approved for a Home Equity Line of Credit (HELOC) meant improving his credit score from 630 to 680 or higher. Thanks to strategic changes and the right guidance, he didn’t just meet that goal – he surpassed it, reaching an impressive 740 in just seven months.

Jose’s story is a great example of how realistic and effective credit rebuilding can be when you’re committed and supported by professionals. It also highlights how even a few targeted actions can make a huge difference.

What Held Him Back

Like many people, Jose had one recent late payment on his credit report. While it might not seem like a major issue, a single late payment can have a significant negative impact – especially if you’re already hovering in the low 600s. Late payments stay on your credit report for up to seven years and can hurt your chances of getting approved for loans, credit cards, or a HELOC.

In addition, Jose’s credit card utilization – the amount of available credit he was using – was sitting at 58%. Experts recommend keeping this number below 30% to show lenders that you can manage credit responsibly. High utilization signals risk, which can drag down your credit score.

What Changed

Working with a nonprofit credit counselor, Jose followed a customized action plan designed to rebuild his credit. His plan focused on two critical changes:

- Removing the late payment: Through the help of his counselor and documentation support, the recent late payment was successfully removed. This step alone helped raise his score and clear a major red flag from his credit history.

- Lowering credit card balances: Jose focused on paying down his credit card debt, reducing his utilization rate from 58% to 46%. While still above the ideal 30%, this improvement helped demonstrate progress – and credit scoring models rewarded him accordingly.

The Result

By July 2024, Jose’s mid-score had jumped from 630 to 740 – a 110-point increase in just seven months. This positioned him not only to qualify for the HELOC he needed, but to do so with much better terms. A higher credit score often means lower interest rates, higher approval amounts, and more financial flexibility.

Why It Matters

Jose’s story proves that credit rebuilding companies that offer personalized, nonprofit support can deliver real results – without gimmicks or empty promises. Unlike the worst credit repair companies that may try to “sweep” your report illegally or charge hidden fees, ethical credit solutions focus on long-term, sustainable changes.

If you’re wondering how credit repair companies remove negative items, the truth is: the good ones don’t “remove” anything illegally. They help you verify the accuracy of your report and dispute errors the right way. They also empower you to make smarter financial choices – like paying down debt and avoiding future late payments.

Ready to Start?

Whether you’ve been denied a loan, are trying to qualify for a HELOC, or just want to stop living with poor credit, our platform connects you with experienced nonprofit credit counselors who know how to help. Credit rebuilding doesn’t have to be scary or expensive – it just has to be smart.